Presentation on the topic of taxation. UK tax system. Types of taxes in the Russian Federation

PRESENTATION ON TAXES AND TAXATION ON THE TOPIC: “TAXES: CLASSIFICATION AND FUNCTIONS” Performed by a student of the AL-DLE-201 group Tatyana Gerasimova

Currently, the types of taxes and fees as the most important component of the tax system are very diverse. Taxes can be classified according to different criteria. All taxes in force on the territory of the Russian Federation, depending on the level of establishment, are divided into three types: federal: regional; local.

Currently, the types of taxes and fees as the most important component of the tax system are very diverse. Taxes can be classified according to different criteria. All taxes in force on the territory of the Russian Federation, depending on the level of establishment, are divided into three types: federal: regional; local.

CLASSIFICATION OF TAXES Federal taxes are established, repealed and amended by the Tax Code of the Russian Federation and are obligatory for payment throughout the territory of the Russian Federation. Regional taxes are established by the Tax Code of the Russian Federation and are obligatory for payment throughout the territory of the relevant constituent entities of the Russian Federation. The government of the constituent entities of the Federation has the right to introduce or abolish regional taxes on its territory and change some elements of taxation in accordance with current federal legislation. Local taxes are regulated by legislative acts of federal authorities and laws of constituent entities of the Russian Federation. In accordance with the Tax Code of the Russian Federation, local government bodies are given the right to introduce or abolish local taxes and fees on the territory of the municipality.

CLASSIFICATION OF TAXES Federal taxes are established, repealed and amended by the Tax Code of the Russian Federation and are obligatory for payment throughout the territory of the Russian Federation. Regional taxes are established by the Tax Code of the Russian Federation and are obligatory for payment throughout the territory of the relevant constituent entities of the Russian Federation. The government of the constituent entities of the Federation has the right to introduce or abolish regional taxes on its territory and change some elements of taxation in accordance with current federal legislation. Local taxes are regulated by legislative acts of federal authorities and laws of constituent entities of the Russian Federation. In accordance with the Tax Code of the Russian Federation, local government bodies are given the right to introduce or abolish local taxes and fees on the territory of the municipality.

Level of establishment Federal Regional Local Taxes Value added tax; Excise taxes; Personal income tax; Corporate income tax; Mineral extraction tax; Water tax; Fees for the use of objects of the animal world and for the use of objects of aquatic biological resources State duty. Organizational property tax; Transport tax; Gambling tax. Land tax; Property tax for individuals.

Level of establishment Federal Regional Local Taxes Value added tax; Excise taxes; Personal income tax; Corporate income tax; Mineral extraction tax; Water tax; Fees for the use of objects of the animal world and for the use of objects of aquatic biological resources State duty. Organizational property tax; Transport tax; Gambling tax. Land tax; Property tax for individuals.

CLASSIFICATION OF TAXES Depending on the method of collection, taxes are divided as follows: direct; indirect.

CLASSIFICATION OF TAXES Depending on the method of collection, taxes are divided as follows: direct; indirect.

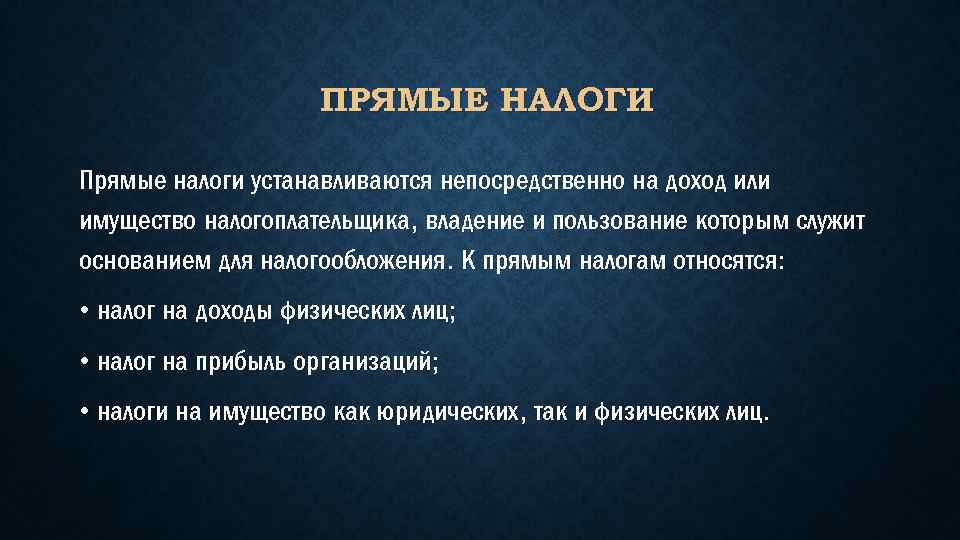

DIRECT TAXES Direct taxes are established directly on the income or property of the taxpayer, the possession and use of which serves as the basis for taxation. Direct taxes include: personal income tax; corporate income tax; property taxes for both legal entities and individuals.

DIRECT TAXES Direct taxes are established directly on the income or property of the taxpayer, the possession and use of which serves as the basis for taxation. Direct taxes include: personal income tax; corporate income tax; property taxes for both legal entities and individuals.

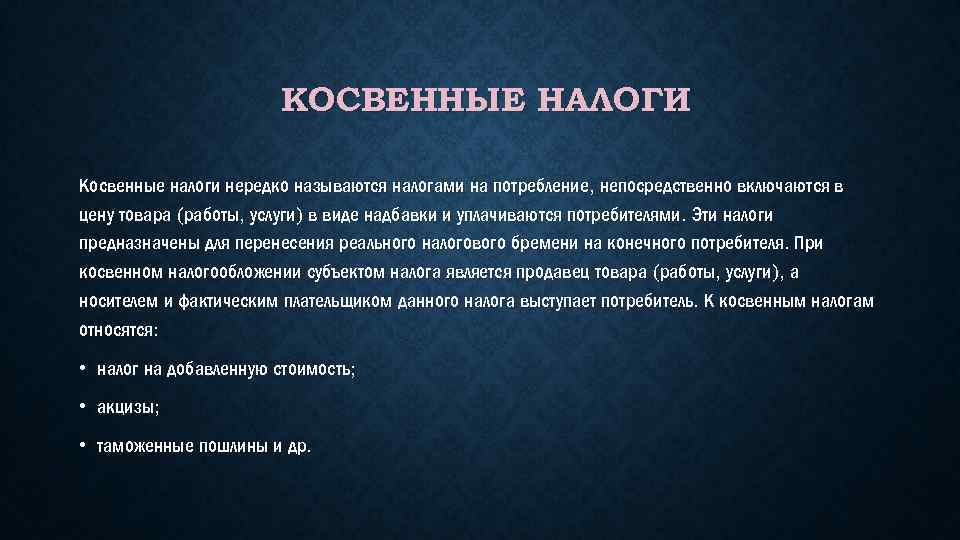

INDIRECT TAXES Indirect taxes are often called consumption taxes; they are directly included in the price of a product (work, service) in the form of a premium and are paid by consumers. These taxes are designed to shift the actual tax burden to the end consumer. With indirect taxation, the subject of the tax is the seller of the product (work, service), and the bearer and actual payer of this tax is the consumer. Indirect taxes include: value added tax; excise taxes; customs duties, etc.

INDIRECT TAXES Indirect taxes are often called consumption taxes; they are directly included in the price of a product (work, service) in the form of a premium and are paid by consumers. These taxes are designed to shift the actual tax burden to the end consumer. With indirect taxation, the subject of the tax is the seller of the product (work, service), and the bearer and actual payer of this tax is the consumer. Indirect taxes include: value added tax; excise taxes; customs duties, etc.

CLASSIFICATION OF TAXES IN THE RF DEPENDING ON THE SUBJECTS OF TAXATION Subject of taxation Taxes paid by legal entities Income tax; Organizational property tax. Taxes paid by individuals Income tax on individuals; Property tax for individuals. Mixed taxes Value added tax; Transport tax; Gambling tax.

CLASSIFICATION OF TAXES IN THE RF DEPENDING ON THE SUBJECTS OF TAXATION Subject of taxation Taxes paid by legal entities Income tax; Organizational property tax. Taxes paid by individuals Income tax on individuals; Property tax for individuals. Mixed taxes Value added tax; Transport tax; Gambling tax.

CLASSIFICATION OF TAXES Depending on the source of payment, taxes are divided into: Taxes attributable to the cost of finished products (works, services): land tax; tax on road users, tax on vehicle owners, fees for the use of natural resources; Taxes, expenses for which are attributed to the proceeds from the sale of products (works, services): VAT; excise taxes; export tariffs; Taxes attributable to profit: income tax; Taxes attributable to other expenses not included in the cost of finished products (works, services): corporate property tax.

CLASSIFICATION OF TAXES Depending on the source of payment, taxes are divided into: Taxes attributable to the cost of finished products (works, services): land tax; tax on road users, tax on vehicle owners, fees for the use of natural resources; Taxes, expenses for which are attributed to the proceeds from the sale of products (works, services): VAT; excise taxes; export tariffs; Taxes attributable to profit: income tax; Taxes attributable to other expenses not included in the cost of finished products (works, services): corporate property tax.

CLASSIFICATION OF TAXES Depending on the applied rates, there are: Fixed taxes. They are characterized by such tax rates, the value of which does not depend on changes in the size of the tax base: VAT, income tax, personal income tax, property tax of organizations, property tax of individuals; Progressive taxes. They are characterized by tax rates, the value of which increases as the tax base increases: excise taxes, transport tax.

CLASSIFICATION OF TAXES Depending on the applied rates, there are: Fixed taxes. They are characterized by such tax rates, the value of which does not depend on changes in the size of the tax base: VAT, income tax, personal income tax, property tax of organizations, property tax of individuals; Progressive taxes. They are characterized by tax rates, the value of which increases as the tax base increases: excise taxes, transport tax.

FUNCTIONS OF TAXES (English tax functions) – stable internal properties, patterns of development and distinctive forms of manifestation that allow us to identify the internal content and purpose of taxes.

FUNCTIONS OF TAXES (English tax functions) – stable internal properties, patterns of development and distinctive forms of manifestation that allow us to identify the internal content and purpose of taxes.

FISCAL FUNCTION OF TAXES The fiscal function follows from the very nature of taxes. It is characteristic of all states in all periods of their existence and development. By implementing this function in practice, state financial resources are formed and material conditions are created for the functioning of the state. The main task of performing the fiscal function is to ensure a stable revenue base for budgets of all levels.

FISCAL FUNCTION OF TAXES The fiscal function follows from the very nature of taxes. It is characteristic of all states in all periods of their existence and development. By implementing this function in practice, state financial resources are formed and material conditions are created for the functioning of the state. The main task of performing the fiscal function is to ensure a stable revenue base for budgets of all levels.

REGULATORY FUNCTION OF TAXES The regulatory function is of particular importance in modern conditions of anti-crisis regulation, active influence of the state on economic and social processes. This function is related in a temporary aspect to the distribution of tax payments between legal entities and individuals, spheres and sectors of the economy, the state as a whole and its territorial entities. This function allows you to regulate the income of different groups of the population. Tax regulation is implemented through a system of benefits and a system of tax payments and fees.

REGULATORY FUNCTION OF TAXES The regulatory function is of particular importance in modern conditions of anti-crisis regulation, active influence of the state on economic and social processes. This function is related in a temporary aspect to the distribution of tax payments between legal entities and individuals, spheres and sectors of the economy, the state as a whole and its territorial entities. This function allows you to regulate the income of different groups of the population. Tax regulation is implemented through a system of benefits and a system of tax payments and fees.

SOCIAL FUNCTION OF TAXES The social function of taxes is closely related to the fiscal and regulatory functions through the conditions for collecting income and property taxes. Taxes are levied in larger amounts on the wealthy, while a significant share of them should go to the poor in the form of social assistance.

SOCIAL FUNCTION OF TAXES The social function of taxes is closely related to the fiscal and regulatory functions through the conditions for collecting income and property taxes. Taxes are levied in larger amounts on the wealthy, while a significant share of them should go to the poor in the form of social assistance.

CONTROL FUNCTION The control function creates the prerequisites for maintaining cost proportions in the process of education and distribution of income of different economic entities. Thanks to it, the effectiveness of each tax channel and the “tax press” as a whole is assessed, and the need to make changes to the tax system and tax policy is identified.

CONTROL FUNCTION The control function creates the prerequisites for maintaining cost proportions in the process of education and distribution of income of different economic entities. Thanks to it, the effectiveness of each tax channel and the “tax press” as a whole is assessed, and the need to make changes to the tax system and tax policy is identified.

Slide 2

Taxes are the price we pay for the opportunity to live in a civilized society. Oliver Wendell Holmes A citizen should pay taxes with the same feeling with which a lover gives gifts to his beloved. Novalis

Slide 3

What is a tax? A tax is a fee levied exclusively by and for the benefit of the state to ensure its functioning (financing public goods). It is charged from both individuals and legal entities. Principles of collection – mandatory, universal, optimal, fair

Slide 4

Chinese interpretation of the word "Tax" Tax in Chinese is 税 (shui). The hieroglyph consists of two parts. The left side means "bread, grain." The right side means "change, pay".

Slide 5

Chinese interpretation of the word "Tax" Combining these two meanings, we have "to pay grain." The very first type of tax was an agricultural tax, which was paid by the crops grown, so the meaning of the word “tax” is obvious. There is another version about the second part of the hieroglyph. According to the Book of Changes, its middle part means a swamp, the two knives at the bottom are the earth, and the two upper features look like waves. That is, it is water on earth. Water symbolizes evenness, impartiality, therefore the hieroglyph “tax” has a connotation of “justice”.

Slide 6

What are the taxes? Federal Regional Local

Slide 7

What are the taxes? Direct Indirect taxes that are levied by the government directly on the income or property of the taxpayer. taxes on goods and services, imposed as a surcharge on a price or tariff, as opposed to direct taxes, determined by the taxpayer's income

Slide 8

Who pays taxes? 1. individuals (income tax of individuals, tax on property of individuals transferred by inheritance or gift, etc.) 2. Organizations (property tax of organizations, income tax of organizations) 3. organizations and individuals (land tax , transport tax, state duty)

Slide 9

How is the money collected in taxes spent? are the main source of national, regional and local (city, district, etc.)

Slide 10

How is the money collected in taxes spent? State and local authorities and management; Taxes support: Armed forces Law enforcement agencies Health care institutions Education, science, culture, art.

Slide 11

How is the money collected in taxes spent? Funds are spent on paying pensions, benefits, subsidies, compensation to pensioners, disabled people, students, low-income large families and other categories of citizens in need of material support and assistance.

Slide 12

I live in the village of Zarya. My village is very beautiful, and in recent years it has become even better. Dawn is getting prettier every day.

Slide 13

On the territory of the village: School

Slide 14

On the territory of the village: Stadium

Slide 15

On the territory of the village: Village Council of the SEC "Druzhba" Civil Registry Office

Slide 16

On the territory of the village: House of Culture

Slide 1

Slide 2

* Legislation on taxes and fees (Article 1 of the Tax Code of the Russian Federation) Legislation of the Russian Federation Tax Code of the Russian Federation and federal laws on taxes and fees adopted in accordance with it Legislation of the constituent entities of the Russian Federation Laws on taxes of the constituent entities of the Russian Federation adopted in accordance with the Tax Code of the Russian Federation Regulatory legal acts of municipal formations Acts on local taxes and fees adopted by the representative bodies of municipalities in accordance with the Tax Code of the Russian Federation The Tax Code of the Russian Federation establishes a system of taxes and fees, as well as general principles of taxation and fees in the Russian Federation, including: - types of taxes and fees levied in the Russian Federation; - the grounds for occurrence (change, termination) and the procedure for fulfilling obligations to pay taxes and fees; - principles of establishing, enacting and terminating previously introduced taxes and fees of constituent entities of the Russian Federation and local taxes and fees; - rights and obligations of taxpayers, tax authorities and other participants in relations regulated by legislation on taxes and fees; - forms and methods of tax control; - responsibility for committing tax offenses; - the procedure for appealing acts of tax authorities and actions (inaction of their officials

* Legislation on taxes and fees (Article 1 of the Tax Code of the Russian Federation) Legislation of the Russian Federation Tax Code of the Russian Federation and federal laws on taxes and fees adopted in accordance with it Legislation of the constituent entities of the Russian Federation Laws on taxes of the constituent entities of the Russian Federation adopted in accordance with the Tax Code of the Russian Federation Regulatory legal acts of municipal formations Acts on local taxes and fees adopted by the representative bodies of municipalities in accordance with the Tax Code of the Russian Federation The Tax Code of the Russian Federation establishes a system of taxes and fees, as well as general principles of taxation and fees in the Russian Federation, including: - types of taxes and fees levied in the Russian Federation; - the grounds for occurrence (change, termination) and the procedure for fulfilling obligations to pay taxes and fees; - principles of establishing, enacting and terminating previously introduced taxes and fees of constituent entities of the Russian Federation and local taxes and fees; - rights and obligations of taxpayers, tax authorities and other participants in relations regulated by legislation on taxes and fees; - forms and methods of tax control; - responsibility for committing tax offenses; - the procedure for appealing acts of tax authorities and actions (inaction of their officials

Slide 3

* Types of taxes and fees in the Russian Federation. Powers of legislative (representative) bodies of state power of the constituent entities of the Russian Federation and representative bodies of municipalities to establish taxes and fees Federal Regional Local When establishing regional taxes, the legislative (representative) bodies of state power of the constituent entities of the Russian Federation are determined in the manner and within the limits provided for by the Tax Code, the following elements of taxation : tax rates, procedure and deadlines for paying taxes. Tax rates for regional taxes are established by the laws of the constituent entities of the Russian Federation within the limits established by the Tax Code. In accordance with paragraph 6 of Art. 12 of the Tax Code of the Russian Federation, federal, regional or local taxes and fees not provided for by the Tax Code of the Russian Federation cannot be established.

* Types of taxes and fees in the Russian Federation. Powers of legislative (representative) bodies of state power of the constituent entities of the Russian Federation and representative bodies of municipalities to establish taxes and fees Federal Regional Local When establishing regional taxes, the legislative (representative) bodies of state power of the constituent entities of the Russian Federation are determined in the manner and within the limits provided for by the Tax Code, the following elements of taxation : tax rates, procedure and deadlines for paying taxes. Tax rates for regional taxes are established by the laws of the constituent entities of the Russian Federation within the limits established by the Tax Code. In accordance with paragraph 6 of Art. 12 of the Tax Code of the Russian Federation, federal, regional or local taxes and fees not provided for by the Tax Code of the Russian Federation cannot be established.

Slide 4

* Taxpayers and payers of fees (Article 19 of the Tax Code of the Russian Federation) Taxpayers and payers of fees are organizations and individuals who, in accordance with the Tax Code, are obliged to pay taxes and fees. Branches and other separate divisions of Russian organizations perform the duties of these organizations to pay taxes and fees at the location of these branches and other separate divisions. Depending on the measurement of the object of taxation, tax rates are expressed: 1) as a percentage of the tax base (income tax, property tax, VAT, etc.) - so-called ad valorem rates; 2) in a fixed amount of money, when a fixed amount of tax payment is established not per unit of taxation (most excise taxes, transport tax) - a specific form; 3) in a combined form, combining fixed and percentage components (tax on property transferred by inheritance or gift, some excise taxes, unified social tax).

* Taxpayers and payers of fees (Article 19 of the Tax Code of the Russian Federation) Taxpayers and payers of fees are organizations and individuals who, in accordance with the Tax Code, are obliged to pay taxes and fees. Branches and other separate divisions of Russian organizations perform the duties of these organizations to pay taxes and fees at the location of these branches and other separate divisions. Depending on the measurement of the object of taxation, tax rates are expressed: 1) as a percentage of the tax base (income tax, property tax, VAT, etc.) - so-called ad valorem rates; 2) in a fixed amount of money, when a fixed amount of tax payment is established not per unit of taxation (most excise taxes, transport tax) - a specific form; 3) in a combined form, combining fixed and percentage components (tax on property transferred by inheritance or gift, some excise taxes, unified social tax).

Slide 5

* Rights and obligations of taxpayers (payers of fees) (Articles 21 and 23 of the Tax Code of the Russian Federation) Rights (Article 21 of the Tax Code of the Russian Federation) Responsibilities (Article 23 of the Tax Code of the Russian Federation) 1) Receive free information from tax authorities at the place of your registration (including in writing) about current taxes and fees; 2) Receive written clarifications from the Ministry of Finance of the Russian Federation on the application of the legislation of the Russian Federation on taxes and fees; 3) for timely offset or refund of amounts of overpaid or overcharged taxes, penalties, and fines; 4) represent your interests in relations regulated by the legislation on taxes and fees, personally or through your representative; 5) provide tax authorities and their officials with explanations on the calculation and payment of taxes, as well as on reports of tax audits carried out; 6) be present during an on-site tax audit; 7) demand that officials of tax authorities and other authorized bodies comply with the legislation on taxes and fees when they carry out actions in relation to taxpayers. 1) Pay legally established taxes; 2) register with the tax authorities, if such an obligation is provided for by the Tax Code of the Russian Federation; 3) submit tax returns (calculations) in accordance with the established procedure to the tax authority at the place of registration, if such an obligation is provided for by the legislation on taxes and fees

* Rights and obligations of taxpayers (payers of fees) (Articles 21 and 23 of the Tax Code of the Russian Federation) Rights (Article 21 of the Tax Code of the Russian Federation) Responsibilities (Article 23 of the Tax Code of the Russian Federation) 1) Receive free information from tax authorities at the place of your registration (including in writing) about current taxes and fees; 2) Receive written clarifications from the Ministry of Finance of the Russian Federation on the application of the legislation of the Russian Federation on taxes and fees; 3) for timely offset or refund of amounts of overpaid or overcharged taxes, penalties, and fines; 4) represent your interests in relations regulated by the legislation on taxes and fees, personally or through your representative; 5) provide tax authorities and their officials with explanations on the calculation and payment of taxes, as well as on reports of tax audits carried out; 6) be present during an on-site tax audit; 7) demand that officials of tax authorities and other authorized bodies comply with the legislation on taxes and fees when they carry out actions in relation to taxpayers. 1) Pay legally established taxes; 2) register with the tax authorities, if such an obligation is provided for by the Tax Code of the Russian Federation; 3) submit tax returns (calculations) in accordance with the established procedure to the tax authority at the place of registration, if such an obligation is provided for by the legislation on taxes and fees

Slide 6

* Tax agents (Article 24 of the Tax Code of the Russian Federation) Tax agents are persons who, in accordance with the Tax Code of the Russian Federation, are entrusted with the responsibility for calculating, withholding from the taxpayer and transferring taxes to the budget system of the Russian Federation. (clause 1 of article 24 of the Tax Code of the Russian Federation) Tax agents are obliged (clause 3 of article 24 of the Tax Code of the Russian Federation): 1) correctly and timely calculate, withhold from funds paid to taxpayers, and transfer taxes to the budget system of the Russian Federation to the appropriate accounts treasury; 2) submit to the tax authority at the place of your registration the documents necessary to monitor the correctness of calculation, withholding and transfer of taxes.

* Tax agents (Article 24 of the Tax Code of the Russian Federation) Tax agents are persons who, in accordance with the Tax Code of the Russian Federation, are entrusted with the responsibility for calculating, withholding from the taxpayer and transferring taxes to the budget system of the Russian Federation. (clause 1 of article 24 of the Tax Code of the Russian Federation) Tax agents are obliged (clause 3 of article 24 of the Tax Code of the Russian Federation): 1) correctly and timely calculate, withhold from funds paid to taxpayers, and transfer taxes to the budget system of the Russian Federation to the appropriate accounts treasury; 2) submit to the tax authority at the place of your registration the documents necessary to monitor the correctness of calculation, withholding and transfer of taxes.

Slide 7

* Object of taxation (Article 38 of the Tax Code of the Russian Federation) Sale of goods (work, services), property, profit, income, expense or other circumstance that has a cost, quantitative or physical characteristic, the presence of which is linked by the legislation on taxes and fees to the emergence of an obligation for the taxpayer on payment of tax

* Object of taxation (Article 38 of the Tax Code of the Russian Federation) Sale of goods (work, services), property, profit, income, expense or other circumstance that has a cost, quantitative or physical characteristic, the presence of which is linked by the legislation on taxes and fees to the emergence of an obligation for the taxpayer on payment of tax

Slide 8

* Collection of taxes, fees, as well as penalties, fines from funds in the accounts of a taxpayer (payer of fees) - an organization, an individual entrepreneur or a tax agent - an organization, an individual entrepreneur in banks (Article 46 of the Tax Code of the Russian Federation) 1. In case of non-payment or In case of incomplete payment of the tax within the established period, the obligation to pay the tax is compulsorily fulfilled by foreclosure on the funds in the accounts of the taxpayer (tax agent). 2. The decision on collection is made after the expiration of the period established in the requirement to pay the tax, but no later than two months after the expiration of the specified period. A decision on collection made after the expiration of the specified period is considered invalid and cannot be executed. In this case, the tax authority may apply to the court with a claim for recovery from the taxpayer (tax agent). 3. If there are insufficient or absent funds in the accounts of the taxpayer (tax agent) - organization or individual entrepreneur, or in the absence of information about the accounts of the taxpayer (tax agent) - organization or individual entrepreneur, the tax authority has the right to collect tax at the expense of other property of the taxpayer (tax agent) .

* Collection of taxes, fees, as well as penalties, fines from funds in the accounts of a taxpayer (payer of fees) - an organization, an individual entrepreneur or a tax agent - an organization, an individual entrepreneur in banks (Article 46 of the Tax Code of the Russian Federation) 1. In case of non-payment or In case of incomplete payment of the tax within the established period, the obligation to pay the tax is compulsorily fulfilled by foreclosure on the funds in the accounts of the taxpayer (tax agent). 2. The decision on collection is made after the expiration of the period established in the requirement to pay the tax, but no later than two months after the expiration of the specified period. A decision on collection made after the expiration of the specified period is considered invalid and cannot be executed. In this case, the tax authority may apply to the court with a claim for recovery from the taxpayer (tax agent). 3. If there are insufficient or absent funds in the accounts of the taxpayer (tax agent) - organization or individual entrepreneur, or in the absence of information about the accounts of the taxpayer (tax agent) - organization or individual entrepreneur, the tax authority has the right to collect tax at the expense of other property of the taxpayer (tax agent) .

Slide 9

* Tax base (Article 53 of the Tax Code of the Russian Federation) - cost, physical and other characteristics of the object of taxation. The tax base and the procedure for determining it for federal, regional and local taxes are established by the Tax Code of the Russian Federation. The tax base is calculated by: Organizations - based on the results of each tax period based on register data accounting and (or) on the basis of other documented data on objects subject to taxation or related to taxation. Individual entrepreneurs, notaries engaged in private practice, lawyers who have established law offices - based on the results of each tax period based on accounting data for income and expenses and business transactions in the manner determined by the Ministry of Finance of the Russian Federation. The same rules apply to tax agents Other taxpayers - individuals - on the basis of information received in established cases from organizations and (or) individuals about the amounts of income paid by them, about the objects of taxation, as well as data from their own accounting of income received, objects of taxation carried out according to arbitrary forms

* Tax base (Article 53 of the Tax Code of the Russian Federation) - cost, physical and other characteristics of the object of taxation. The tax base and the procedure for determining it for federal, regional and local taxes are established by the Tax Code of the Russian Federation. The tax base is calculated by: Organizations - based on the results of each tax period based on register data accounting and (or) on the basis of other documented data on objects subject to taxation or related to taxation. Individual entrepreneurs, notaries engaged in private practice, lawyers who have established law offices - based on the results of each tax period based on accounting data for income and expenses and business transactions in the manner determined by the Ministry of Finance of the Russian Federation. The same rules apply to tax agents Other taxpayers - individuals - on the basis of information received in established cases from organizations and (or) individuals about the amounts of income paid by them, about the objects of taxation, as well as data from their own accounting of income received, objects of taxation carried out according to arbitrary forms

Slide 10

* Tax period (Article 55 of the Tax Code of the Russian Federation) The tax period means a calendar year or another period of time in relation to individual taxes, at the end of which the tax base is determined and the amount of tax payable is calculated. Establishment and use of benefits for taxes and fees (Article 56 of the Tax Code of the Russian Federation) Benefits for taxes and fees are recognized as the benefits provided to certain categories of taxpayers and payers of fees provided for by the legislation on taxes and fees in comparison with other taxpayers or payers of fees, including the opportunity not to pay taxes or fee or pay them in a smaller amount. The norms of legislation on taxes and fees that determine the grounds, procedure and conditions for applying tax benefits and fees cannot be of an individual nature.

* Tax period (Article 55 of the Tax Code of the Russian Federation) The tax period means a calendar year or another period of time in relation to individual taxes, at the end of which the tax base is determined and the amount of tax payable is calculated. Establishment and use of benefits for taxes and fees (Article 56 of the Tax Code of the Russian Federation) Benefits for taxes and fees are recognized as the benefits provided to certain categories of taxpayers and payers of fees provided for by the legislation on taxes and fees in comparison with other taxpayers or payers of fees, including the opportunity not to pay taxes or fee or pay them in a smaller amount. The norms of legislation on taxes and fees that determine the grounds, procedure and conditions for applying tax benefits and fees cannot be of an individual nature.

Slide 11

* Registration of organizations and individuals (Article 83 of the Tax Code of the Russian Federation) For the purpose of tax control, organizations and individuals are subject to registration with the tax authorities at the location of the organization, the location of its separate divisions, the place of residence of the individual, as well as at the location real estate and vehicles owned by them.

* Registration of organizations and individuals (Article 83 of the Tax Code of the Russian Federation) For the purpose of tax control, organizations and individuals are subject to registration with the tax authorities at the location of the organization, the location of its separate divisions, the place of residence of the individual, as well as at the location real estate and vehicles owned by them.

Slide 12

* Tax audits (Articles 88 and 89 of the Tax Code of the Russian Federation) Types of tax audits Desk tax audit On-site tax audit Desk tax audit (Article 88 of the Tax Code of the Russian Federation) Desk tax audit is carried out: - at the location of the tax authority on the basis of tax returns (calculations) and documents submitted by the taxpayer, as well as other documents on the activities of the taxpayer available to the tax authority; - authorized officials of the tax authority in accordance with their official duties without any special decision of the head of the tax authority within three months from the date of submission by the taxpayer (payer of fees, tax agent) of the tax return (calculations) and documents that, in accordance with the Tax Code of the Russian Federation must be attached to the tax return. On-site tax audit (Article 89 of the Tax Code of the Russian Federation) On-site tax audit is carried out on the territory (premises) of the taxpayer based on the decision of the head (deputy head) of the tax authority. An on-site tax audit cannot last more than two months.

* Tax audits (Articles 88 and 89 of the Tax Code of the Russian Federation) Types of tax audits Desk tax audit On-site tax audit Desk tax audit (Article 88 of the Tax Code of the Russian Federation) Desk tax audit is carried out: - at the location of the tax authority on the basis of tax returns (calculations) and documents submitted by the taxpayer, as well as other documents on the activities of the taxpayer available to the tax authority; - authorized officials of the tax authority in accordance with their official duties without any special decision of the head of the tax authority within three months from the date of submission by the taxpayer (payer of fees, tax agent) of the tax return (calculations) and documents that, in accordance with the Tax Code of the Russian Federation must be attached to the tax return. On-site tax audit (Article 89 of the Tax Code of the Russian Federation) On-site tax audit is carried out on the territory (premises) of the taxpayer based on the decision of the head (deputy head) of the tax authority. An on-site tax audit cannot last more than two months.

Slide 13

* Types of tax offenses and liability for their commission Type of offense Amount of fine Taxpayers and other persons Violation of the deadline for filing an application for registration with the tax authority (Article 116 of the Tax Code of the Russian Federation): - up to 90 calendar days - over 90 calendar days 5 thousand rubles . 10 thousand rubles. Failure to submit a tax return on time: - up to 180 days (inclusive) upon expiration of the established period (clause 1 of Article 119 of the Tax Code of the Russian Federation) 5% of the amount of tax subject to additional payment) based on this declaration, for each month from the date established for its presentation, for no more than 30% of the indicated amount and no more than 100 rubles. - more than 180 days after the expiration of the established period (clause 2 of Article 119 of the Tax Code of the Russian Federation) 30% of the total amount of tax payable on the basis of this declaration, and 10% of the amount of tax payable on the basis of this declaration, for each month starting from 181 -th day

* Types of tax offenses and liability for their commission Type of offense Amount of fine Taxpayers and other persons Violation of the deadline for filing an application for registration with the tax authority (Article 116 of the Tax Code of the Russian Federation): - up to 90 calendar days - over 90 calendar days 5 thousand rubles . 10 thousand rubles. Failure to submit a tax return on time: - up to 180 days (inclusive) upon expiration of the established period (clause 1 of Article 119 of the Tax Code of the Russian Federation) 5% of the amount of tax subject to additional payment) based on this declaration, for each month from the date established for its presentation, for no more than 30% of the indicated amount and no more than 100 rubles. - more than 180 days after the expiration of the established period (clause 2 of Article 119 of the Tax Code of the Russian Federation) 30% of the total amount of tax payable on the basis of this declaration, and 10% of the amount of tax payable on the basis of this declaration, for each month starting from 181 -th day

Slide 14

* Type of offense Amount of fine Taxpayers and other persons Gross violation of the rules for accounting for income and (or) expenses and (or) objects of taxation (Article 120 of the Tax Code of the Russian Federation): - if these acts were committed during one tax period; - if these acts were committed during more than one tax period; - if they resulted in an understatement of the tax base - 5 thousand rubles. - 15 thousand rubles. - 10% of the amount of unpaid tax, but not less than 15 thousand rubles. Non-payment or incomplete payment of tax (fee) amounts as a result of understatement of the tax base, other incorrect calculation of tax (fee) or other unlawful actions (inaction) (clause 1 of Article 122 of the Tax Code of the Russian Federation); - also an act committed intentionally (clause 3 of Article 122 of the Tax Code of the Russian Federation) - 20% of the unpaid amount of tax (fee) - 40% of the unpaid amount of tax (fee) Illegal non-transfer (incomplete transfer) of tax amounts subject to withholding and transfer by the tax agent (Article 123 of the Tax Code of the Russian Federation) - 20% of the amount to be transferred

* Type of offense Amount of fine Taxpayers and other persons Gross violation of the rules for accounting for income and (or) expenses and (or) objects of taxation (Article 120 of the Tax Code of the Russian Federation): - if these acts were committed during one tax period; - if these acts were committed during more than one tax period; - if they resulted in an understatement of the tax base - 5 thousand rubles. - 15 thousand rubles. - 10% of the amount of unpaid tax, but not less than 15 thousand rubles. Non-payment or incomplete payment of tax (fee) amounts as a result of understatement of the tax base, other incorrect calculation of tax (fee) or other unlawful actions (inaction) (clause 1 of Article 122 of the Tax Code of the Russian Federation); - also an act committed intentionally (clause 3 of Article 122 of the Tax Code of the Russian Federation) - 20% of the unpaid amount of tax (fee) - 40% of the unpaid amount of tax (fee) Illegal non-transfer (incomplete transfer) of tax amounts subject to withholding and transfer by the tax agent (Article 123 of the Tax Code of the Russian Federation) - 20% of the amount to be transferred

Slide 15

Slide 16

* Taxpayers (Article 143 of the Tax Code of the Russian Federation) Organizations Individual entrepreneurs Except - those using a simplified taxation system; - transferred to the payment of a single tax on imputed income; - transferred to the payment of the unified agricultural tax. Exemption from the performance of taxpayer obligations (Article 145 of the Tax Code of the Russian Federation) Organizations and individual entrepreneurs have the right to exemption from the performance of taxpayer obligations related to the calculation and payment of VAT, if for the three consecutive calendar months preceding such exemption the amount of revenue from the sale of goods (works, services) ) excluding VAT did not exceed 2 million rubles in total.

* Taxpayers (Article 143 of the Tax Code of the Russian Federation) Organizations Individual entrepreneurs Except - those using a simplified taxation system; - transferred to the payment of a single tax on imputed income; - transferred to the payment of the unified agricultural tax. Exemption from the performance of taxpayer obligations (Article 145 of the Tax Code of the Russian Federation) Organizations and individual entrepreneurs have the right to exemption from the performance of taxpayer obligations related to the calculation and payment of VAT, if for the three consecutive calendar months preceding such exemption the amount of revenue from the sale of goods (works, services) ) excluding VAT did not exceed 2 million rubles in total.

Slide 17

* Tax period (Article 163 of the Tax Code of the Russian Federation) The tax period (including for taxpayers acting as tax agents, hereinafter referred to as tax agents) is established as a quarter.

* Tax period (Article 163 of the Tax Code of the Russian Federation) The tax period (including for taxpayers acting as tax agents, hereinafter referred to as tax agents) is established as a quarter.

Slide 18

* Value added tax rates (Article 164 of the Tax Code of the Russian Federation) Goods exported under the customs regime of export or placed under the customs regime of a free customs zone, subject to the submission of established documents to the tax authorities, as well as work (services) directly related to production and sales of these goods. Some food products, products for children, periodicals, books, medical products. Other goods (works, services) 0% 10% 18%

* Value added tax rates (Article 164 of the Tax Code of the Russian Federation) Goods exported under the customs regime of export or placed under the customs regime of a free customs zone, subject to the submission of established documents to the tax authorities, as well as work (services) directly related to production and sales of these goods. Some food products, products for children, periodicals, books, medical products. Other goods (works, services) 0% 10% 18%

Slide 19

* Object of taxation (Article 146 of the Tax Code of the Russian Federation) Sale on the territory of the Russian Federation of goods, work performed and services provided, including the sale of pledged items and transfer of goods (results of work performed, provision of services) under an agreement on the provision of compensation or novation, as well as transfer property rights Transfer of goods on the territory of the Russian Federation (performance of work, provision of services) for one’s own needs, expenses for which are not deductible (including through depreciation deductions) when calculating an organization’s income tax Import of goods into the customs territory of the Russian Federation Carrying out construction and installation work for own consumption

* Object of taxation (Article 146 of the Tax Code of the Russian Federation) Sale on the territory of the Russian Federation of goods, work performed and services provided, including the sale of pledged items and transfer of goods (results of work performed, provision of services) under an agreement on the provision of compensation or novation, as well as transfer property rights Transfer of goods on the territory of the Russian Federation (performance of work, provision of services) for one’s own needs, expenses for which are not deductible (including through depreciation deductions) when calculating an organization’s income tax Import of goods into the customs territory of the Russian Federation Carrying out construction and installation work for own consumption

Slide 20

* Transactions not subject to taxation (exempt from taxation) art. 149 of the Tax Code of the Russian Federation The sale (as well as the transfer, execution, provision for one’s own needs) on the territory of the Russian Federation is not subject to taxation (exempt from taxation): - shares in the authorized (share) capital of organizations, shares in mutual funds of cooperatives and mutual investment funds, valuable securities and derivatives instruments (including forwards, futures contracts, options). Value added tax is not levied on income from the sale of securities by an investor organization and income from the sale of government securities by a dealer. Transactions on the sale of bills of exchange are not subject to VAT.

* Transactions not subject to taxation (exempt from taxation) art. 149 of the Tax Code of the Russian Federation The sale (as well as the transfer, execution, provision for one’s own needs) on the territory of the Russian Federation is not subject to taxation (exempt from taxation): - shares in the authorized (share) capital of organizations, shares in mutual funds of cooperatives and mutual investment funds, valuable securities and derivatives instruments (including forwards, futures contracts, options). Value added tax is not levied on income from the sale of securities by an investor organization and income from the sale of government securities by a dealer. Transactions on the sale of bills of exchange are not subject to VAT.

Slide 21

Slide 22

* Taxpayers and objects of taxation (Articles 207 and 209 of the Tax Code of the Russian Federation) Taxpayers Individuals who are tax residents of the Russian Federation (individuals who are actually in the Russian Federation for at least 183 calendar days within 12 consecutive months. The period of stay in the Russian Federation is not interrupted by period of departure outside the Russian Federation for short-term (less than six months) treatment or training Individuals receiving income from sources in the Russian Federation who are not tax residents of the Russian Federation (individuals actually staying in the territory of the Russian Federation for less than 183 days in a calendar year) Objects of taxation Income from sources in the Russian Federation and outside the Russian Federation Income received from sources in the Russian Federation Income from transactions related to property and non-property relations of individuals recognized as family members and (or) close relatives in accordance with the Family Code of the Russian Federation is not recognized as income. with the exception of income received by these individuals as a result of the conclusion of civil law contracts or labor relations between these persons. Tax period (Art. 216 of the Tax Code of the Russian Federation) The tax period is the calendar year

* Taxpayers and objects of taxation (Articles 207 and 209 of the Tax Code of the Russian Federation) Taxpayers Individuals who are tax residents of the Russian Federation (individuals who are actually in the Russian Federation for at least 183 calendar days within 12 consecutive months. The period of stay in the Russian Federation is not interrupted by period of departure outside the Russian Federation for short-term (less than six months) treatment or training Individuals receiving income from sources in the Russian Federation who are not tax residents of the Russian Federation (individuals actually staying in the territory of the Russian Federation for less than 183 days in a calendar year) Objects of taxation Income from sources in the Russian Federation and outside the Russian Federation Income received from sources in the Russian Federation Income from transactions related to property and non-property relations of individuals recognized as family members and (or) close relatives in accordance with the Family Code of the Russian Federation is not recognized as income. with the exception of income received by these individuals as a result of the conclusion of civil law contracts or labor relations between these persons. Tax period (Art. 216 of the Tax Code of the Russian Federation) The tax period is the calendar year

Slide 23

* Tax base for personal income tax (Article 210 of the Tax Code of the Russian Federation) Income in kind Tax base Income in cash + + + Income, the right to dispose of which has arisen Material benefit

* Tax base for personal income tax (Article 210 of the Tax Code of the Russian Federation) Income in kind Tax base Income in cash + + + Income, the right to dispose of which has arisen Material benefit

Slide 24

* Peculiarities of determining the tax base when receiving income in the form of material benefits (Article 212 of the Tax Code of the Russian Federation) The taxpayer’s income received in the form of material benefits is: - material benefits received from savings on interest for the taxpayer’s use of borrowed (credit) funds received from organizations or individual entrepreneurs; - material benefit received from the acquisition of goods (work, services) in accordance with a civil contract from individuals, organizations and individual entrepreneurs who are interdependent in relation to the taxpayer; - material benefit received from the acquisition of securities. When a taxpayer receives income in the form of material benefits from the acquisition of securities, the tax base is determined as the excess of the market value of the securities, determined taking into account the maximum limit of fluctuations in the market price of the securities, over the amount of the taxpayer's actual expenses for their acquisition. The procedure for determining the market price of securities and the maximum limit for fluctuations in the market price of securities is established by the federal body that regulates the securities market.

* Peculiarities of determining the tax base when receiving income in the form of material benefits (Article 212 of the Tax Code of the Russian Federation) The taxpayer’s income received in the form of material benefits is: - material benefits received from savings on interest for the taxpayer’s use of borrowed (credit) funds received from organizations or individual entrepreneurs; - material benefit received from the acquisition of goods (work, services) in accordance with a civil contract from individuals, organizations and individual entrepreneurs who are interdependent in relation to the taxpayer; - material benefit received from the acquisition of securities. When a taxpayer receives income in the form of material benefits from the acquisition of securities, the tax base is determined as the excess of the market value of the securities, determined taking into account the maximum limit of fluctuations in the market price of the securities, over the amount of the taxpayer's actual expenses for their acquisition. The procedure for determining the market price of securities and the maximum limit for fluctuations in the market price of securities is established by the federal body that regulates the securities market.

Slide 25

* A deduction in the amount of actually incurred and documented expenses is provided to the taxpayer When calculating and paying to the budget at the source of payment of income or at the end of the tax period and filing a tax return with the tax authority. Loss on transactions with securities traded on the organized securities market, received by the results of these transactions performed in the tax period, reduces the tax base for transactions of purchase and sale of securities of this category.

* A deduction in the amount of actually incurred and documented expenses is provided to the taxpayer When calculating and paying to the budget at the source of payment of income or at the end of the tax period and filing a tax return with the tax authority. Loss on transactions with securities traded on the organized securities market, received by the results of these transactions performed in the tax period, reduces the tax base for transactions of purchase and sale of securities of this category.

Slide 26

* Payment of funds for the purpose of determining the tax base for personal income tax means: Payment of cash Transfer of funds to the bank account of an individual Transfer of funds to the account of a third party at the request of an individual

* Payment of funds for the purpose of determining the tax base for personal income tax means: Payment of cash Transfer of funds to the bank account of an individual Transfer of funds to the account of a third party at the request of an individual

Slide 27

* Peculiarities of determining the tax base when receiving income in the form of interest received on deposits in banks (Article 214.2 of the Tax Code of the Russian Federation): In relation to income in the form of interest received on deposits in banks, the tax base is determined as the excess of the amount of interest accrued in accordance with terms of the agreement, above the amount of interest calculated on ruble deposits based on the refinancing rate of the Central Bank of the Russian Federation, valid during the period for which the specified interest was accrued, and on deposits in foreign currency based on 9 percent per annum, unless otherwise provided by Chapter 23.

* Peculiarities of determining the tax base when receiving income in the form of interest received on deposits in banks (Article 214.2 of the Tax Code of the Russian Federation): In relation to income in the form of interest received on deposits in banks, the tax base is determined as the excess of the amount of interest accrued in accordance with terms of the agreement, above the amount of interest calculated on ruble deposits based on the refinancing rate of the Central Bank of the Russian Federation, valid during the period for which the specified interest was accrued, and on deposits in foreign currency based on 9 percent per annum, unless otherwise provided by Chapter 23.

Slide 28

* Income not subject to taxation (Article 217 of the Tax Code of the Russian Federation) Shares received by the spouse as a gift from the spouse Amounts of interest on government securities Amounts of interest on bonds of constituent entities of the Russian Federation Amounts of interest on bonds of local self-government bodies Income received from a joint-stock company by a shareholder of this company in the form of additional shares issued as a result of revaluation of JSC fixed assets Income in the form of interest on bank deposits (in rubles) within the discount rate of the Bank of Russia

* Income not subject to taxation (Article 217 of the Tax Code of the Russian Federation) Shares received by the spouse as a gift from the spouse Amounts of interest on government securities Amounts of interest on bonds of constituent entities of the Russian Federation Amounts of interest on bonds of local self-government bodies Income received from a joint-stock company by a shareholder of this company in the form of additional shares issued as a result of revaluation of JSC fixed assets Income in the form of interest on bank deposits (in rubles) within the discount rate of the Bank of Russia

Slide 29

* Tax rate on personal income Tax rate Income for which a tax rate is established Rates on income received by tax residents of the Russian Federation The value of any winnings and prizes received in competitions, games and other events for the purpose of advertising goods, works and services, in parts of the excess of 4,000 rubles. for the tax period Interest income on deposits in banks in terms of excess amounts calculated for ruble deposits based on the refinancing rate of the Central Bank of the Russian Federation, valid during the period for which the specified interest was accrued, and for deposits in foreign currency based on 9 percent per annum, unless otherwise provided by this chapter. Amounts of savings on interest when taxpayers receive borrowed (credit) funds in terms of excess amounts calculated on the basis of three-quarters of the refinancing rate of the Central Bank of the Russian Federation and the interest rate under the agreement for the use of borrowed (credit) funds (for foreign currency accounts - based on 9%), for with the exception of material benefits received from savings on interest for the use by taxpayers of targeted loans and (credits) received from credit and other organizations of the Russian Federation. In relation to income from equity participation in the activities of organizations received in the form of dividends by individuals In relation to income in the form of interest on mortgage-backed bonds issued before January 1, 2007, as well as on income of the founders of trust management of mortgage coverage received on the basis of the acquisition of mortgage-backed participation certificates issued by the mortgage coverage manager before January 1, 2007. All other income not specified above 35% 9% 13% Rates on income received by tax non-residents of the Russian Federation In relation to all income received by individuals who are not tax residents of the Russian Federation, with the exception of income received in the form of dividends from equity participation in activities Russian organizations in respect of which the tax rate is set at 15 percent. thirty %

* Tax rate on personal income Tax rate Income for which a tax rate is established Rates on income received by tax residents of the Russian Federation The value of any winnings and prizes received in competitions, games and other events for the purpose of advertising goods, works and services, in parts of the excess of 4,000 rubles. for the tax period Interest income on deposits in banks in terms of excess amounts calculated for ruble deposits based on the refinancing rate of the Central Bank of the Russian Federation, valid during the period for which the specified interest was accrued, and for deposits in foreign currency based on 9 percent per annum, unless otherwise provided by this chapter. Amounts of savings on interest when taxpayers receive borrowed (credit) funds in terms of excess amounts calculated on the basis of three-quarters of the refinancing rate of the Central Bank of the Russian Federation and the interest rate under the agreement for the use of borrowed (credit) funds (for foreign currency accounts - based on 9%), for with the exception of material benefits received from savings on interest for the use by taxpayers of targeted loans and (credits) received from credit and other organizations of the Russian Federation. In relation to income from equity participation in the activities of organizations received in the form of dividends by individuals In relation to income in the form of interest on mortgage-backed bonds issued before January 1, 2007, as well as on income of the founders of trust management of mortgage coverage received on the basis of the acquisition of mortgage-backed participation certificates issued by the mortgage coverage manager before January 1, 2007. All other income not specified above 35% 9% 13% Rates on income received by tax non-residents of the Russian Federation In relation to all income received by individuals who are not tax residents of the Russian Federation, with the exception of income received in the form of dividends from equity participation in activities Russian organizations in respect of which the tax rate is set at 15 percent. thirty %

Slide 30

* Examples of solving personal income tax problems An individual is given interest on a savings certificate in the amount of 15% per annum. The refinancing rate of the Bank of Russia is 12% per annum. The amount of accrued interest is 2 thousand rubles. Determine the amount of personal income tax on interest. Answer: Let’s make a proportion of 2,000 x 12% / 15% = 1,600 rubles; 2000 rub. - 1600 rub. = 400 rub.; 400 x 35% = 140 rub. The JSC accrued dividends to individuals for 2007. Shareholder Ivanov, who works at the JSC, received 1 thousand rubles; shareholder Petrov, a former employee, - 2 thousand rubles. Currently, Petrov permanently resides in Ukraine. Determine the total amount of personal income tax transferred by the joint-stock company to the budget. Answer: The total tax amount is 390 rubles. (1000 x 9% = 90 rubles; 2000 x 15% = 300 rubles; 90 + 300 = 390 rubles) The total amount of profit tax and personal income tax subject to withholding from the income of dividend recipients - tax residents of the Russian Federation Federation, equal to 100 thousand rubles. The share of legal entity JSC "A" in the total amount of dividends is equal to 20%, the share of individual B. in the total amount of dividends is equal to 10%. Determine the amount of tax to be withheld from the income of dividend recipients of JSC "A" and B. Answer: The amount of tax on dividends of JSC "A" is 20 thousand rubles. (100 thousand rubles x 20%), from dividends of individual B. - 10 thousand rubles. (100 thousand rubles x 10%).

* Examples of solving personal income tax problems An individual is given interest on a savings certificate in the amount of 15% per annum. The refinancing rate of the Bank of Russia is 12% per annum. The amount of accrued interest is 2 thousand rubles. Determine the amount of personal income tax on interest. Answer: Let’s make a proportion of 2,000 x 12% / 15% = 1,600 rubles; 2000 rub. - 1600 rub. = 400 rub.; 400 x 35% = 140 rub. The JSC accrued dividends to individuals for 2007. Shareholder Ivanov, who works at the JSC, received 1 thousand rubles; shareholder Petrov, a former employee, - 2 thousand rubles. Currently, Petrov permanently resides in Ukraine. Determine the total amount of personal income tax transferred by the joint-stock company to the budget. Answer: The total tax amount is 390 rubles. (1000 x 9% = 90 rubles; 2000 x 15% = 300 rubles; 90 + 300 = 390 rubles) The total amount of profit tax and personal income tax subject to withholding from the income of dividend recipients - tax residents of the Russian Federation Federation, equal to 100 thousand rubles. The share of legal entity JSC "A" in the total amount of dividends is equal to 20%, the share of individual B. in the total amount of dividends is equal to 10%. Determine the amount of tax to be withheld from the income of dividend recipients of JSC "A" and B. Answer: The amount of tax on dividends of JSC "A" is 20 thousand rubles. (100 thousand rubles x 20%), from dividends of individual B. - 10 thousand rubles. (100 thousand rubles x 10%).

Slide 31

* Examples of solving problems regarding personal income tax The tax base determined by income received in the form of dividends from a Russian organization by tax residents of the Russian Federation is equal to 200 thousand rubles. Determine the total amount of tax to be withheld from the income of dividend recipients. Answer: The total tax amount is 18 thousand rubles. (200 thousand rubles x 9%) The security of JSC "A" was purchased by an individual for 800 rubles. The market value of the security price, determined taking into account the maximum fluctuation limit of the market price of JSC "A" securities, is 900 rubles. Determine the amount of personal income tax. Answer: The tax amount is 13 rubles. ((900 rub. - 800 rub.) x 13%). An individual purchased shares of JSC "A" for 100 rubles, paying a registration fee of 10 rubles, and then sold them for 150 rubles, paying a commission of 10 rubles to the broker. Determine the amount of personal income tax due on income received. Answer: The tax amount is 4 rubles. (100 rubles + 10 rubles = 110 rubles; 150 rubles - 110 rubles = 40 rubles; 40 rubles - 10 rubles = 30 rubles; 30 rubles x 13% = 4 rubles. The joint-stock company accrued dividends to its shareholders Petrov, a citizen of Ukraine permanently residing there, was accrued 10 thousand rubles; shareholder Tereshchenko, a resident of the Russian Federation, was also accrued 10 thousand rubles. Determine the total amount of income tax withheld by the tax agent: Answer: The total amount of tax is 2,400. rub. (10 thousand rubles x 15% = 1,500 rubles; 10 thousand rubles x 9% = 900 rubles; 1,500 rubles + 900 rubles = 2,400 rubles)

* Examples of solving problems regarding personal income tax The tax base determined by income received in the form of dividends from a Russian organization by tax residents of the Russian Federation is equal to 200 thousand rubles. Determine the total amount of tax to be withheld from the income of dividend recipients. Answer: The total tax amount is 18 thousand rubles. (200 thousand rubles x 9%) The security of JSC "A" was purchased by an individual for 800 rubles. The market value of the security price, determined taking into account the maximum fluctuation limit of the market price of JSC "A" securities, is 900 rubles. Determine the amount of personal income tax. Answer: The tax amount is 13 rubles. ((900 rub. - 800 rub.) x 13%). An individual purchased shares of JSC "A" for 100 rubles, paying a registration fee of 10 rubles, and then sold them for 150 rubles, paying a commission of 10 rubles to the broker. Determine the amount of personal income tax due on income received. Answer: The tax amount is 4 rubles. (100 rubles + 10 rubles = 110 rubles; 150 rubles - 110 rubles = 40 rubles; 40 rubles - 10 rubles = 30 rubles; 30 rubles x 13% = 4 rubles. The joint-stock company accrued dividends to its shareholders Petrov, a citizen of Ukraine permanently residing there, was accrued 10 thousand rubles; shareholder Tereshchenko, a resident of the Russian Federation, was also accrued 10 thousand rubles. Determine the total amount of income tax withheld by the tax agent: Answer: The total amount of tax is 2,400. rub. (10 thousand rubles x 15% = 1,500 rubles; 10 thousand rubles x 9% = 900 rubles; 1,500 rubles + 900 rubles = 2,400 rubles)

Slide 32

Slide 33

* Taxpayers (Article 246 of the Tax Code of the Russian Federation) Russian organizations are not taxpayers; organizations transferred to pay a single tax on imputed income and organizations applying a simplified tax system Foreign organizations - Carrying out their activities in the Russian Federation through permanent representative offices; - receiving income from sources in the Russian Federation Tax and reporting periods (Article 285 of the Tax Code of the Russian Federation) The tax period for tax is the calendar year. Reporting periods for tax are: - for taxpayers calculating monthly advance payments based on actual profit - a month, two months and etc. before the end of the calendar year; - for other taxpayers - the first quarter, six months and nine months of the calendar year.

* Taxpayers (Article 246 of the Tax Code of the Russian Federation) Russian organizations are not taxpayers; organizations transferred to pay a single tax on imputed income and organizations applying a simplified tax system Foreign organizations - Carrying out their activities in the Russian Federation through permanent representative offices; - receiving income from sources in the Russian Federation Tax and reporting periods (Article 285 of the Tax Code of the Russian Federation) The tax period for tax is the calendar year. Reporting periods for tax are: - for taxpayers calculating monthly advance payments based on actual profit - a month, two months and etc. before the end of the calendar year; - for other taxpayers - the first quarter, six months and nine months of the calendar year.

Slide 34

* Profit tax rate Tax rate Income for which the tax rate is established Tax rates on income of foreign organizations not related to activities in the Russian Federation through a permanent establishment For all income, taking into account the provisions of Art. 310 of the Tax Code of the Russian Federation from the use, maintenance or rental (charter) of ships, aircraft or other mobile vehicles or containers (including trailers and auxiliary equipment necessary for transportation) in connection with international transport. 20% 10% Tax base determined on income received in the form of dividends For income received by Russian organizations in the form of dividends, provided that on the day the decision to pay dividends is made, the organization receiving dividends has continuously owned for at least 365 days less than 50 percent contribution (shares) in the authorized (share) capital (fund) of the organization paying dividends or depositary receipts giving the right to receive dividends in an amount corresponding to at least 50 percent of the total amount of dividends paid by the organization, and provided that the cost of acquiring and (or) receiving, in accordance with the legislation of the Russian Federation, ownership of a contribution (share) in the authorized (share) capital (fund) of an organization paying dividends or depositary receipts giving the right to receive dividends exceeds 500 million rubles. For income received in the form of dividends from Russian and foreign organizations by Russian organizations. For income received in the form of dividends from Russian organizations by foreign organizations. 0% 9% 15%

* Profit tax rate Tax rate Income for which the tax rate is established Tax rates on income of foreign organizations not related to activities in the Russian Federation through a permanent establishment For all income, taking into account the provisions of Art. 310 of the Tax Code of the Russian Federation from the use, maintenance or rental (charter) of ships, aircraft or other mobile vehicles or containers (including trailers and auxiliary equipment necessary for transportation) in connection with international transport. 20% 10% Tax base determined on income received in the form of dividends For income received by Russian organizations in the form of dividends, provided that on the day the decision to pay dividends is made, the organization receiving dividends has continuously owned for at least 365 days less than 50 percent contribution (shares) in the authorized (share) capital (fund) of the organization paying dividends or depositary receipts giving the right to receive dividends in an amount corresponding to at least 50 percent of the total amount of dividends paid by the organization, and provided that the cost of acquiring and (or) receiving, in accordance with the legislation of the Russian Federation, ownership of a contribution (share) in the authorized (share) capital (fund) of an organization paying dividends or depositary receipts giving the right to receive dividends exceeds 500 million rubles. For income received in the form of dividends from Russian and foreign organizations by Russian organizations. For income received in the form of dividends from Russian organizations by foreign organizations. 0% 9% 15%

Slide 35

Slide 36

* State duty State duty (Article 333.16 of the Tax Code of the Russian Federation) is a fee levied on persons who are its payers when they apply to state bodies, local governments, other bodies and (or) officials who are authorized in accordance with legislative acts of the Russian Federation, legislative acts of constituent entities of the Russian Federation and normative legal acts of local self-government bodies, for the performance of legally significant actions in relation to these persons, with the exception of actions performed by consular offices of the Russian Federation. Payers of state duties are recognized as organizations and individuals if they apply for legally significant actions or act as defendants in courts of general jurisdiction, arbitration courts or in cases considered by magistrates, and if the court decision is not made in their favor and the plaintiff is exempt from payment of state duty in accordance with this chapter.

* State duty State duty (Article 333.16 of the Tax Code of the Russian Federation) is a fee levied on persons who are its payers when they apply to state bodies, local governments, other bodies and (or) officials who are authorized in accordance with legislative acts of the Russian Federation, legislative acts of constituent entities of the Russian Federation and normative legal acts of local self-government bodies, for the performance of legally significant actions in relation to these persons, with the exception of actions performed by consular offices of the Russian Federation. Payers of state duties are recognized as organizations and individuals if they apply for legally significant actions or act as defendants in courts of general jurisdiction, arbitration courts or in cases considered by magistrates, and if the court decision is not made in their favor and the plaintiff is exempt from payment of state duty in accordance with this chapter.

Slide 37

REPUBLICAN PRESENTATION COMPETITION “TAXES THROUGH THE EYES OF SCHOOLCHILDREN” RELEVANCE OF THE TOPIC

Russian tax system

Structure of Russian tax authorities

TAX HISTORY

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

FUNCTIONS AND TYPES OF TAXES IN THE RF

Functions of taxes:

The functions of taxes show how the social purpose of taxes is realized as an instrument of cost distribution and redistribution of income. Fiscal;

Regulatory;

Distribution;

Control;

Stimulating

TYPES OF TAXES IN THE RF

MAIN TYPES OF TAXES IN THE RF

Direct and indirect

. Direct taxes are levied directly on the taxpayer's property or income. These taxes are divided into real direct taxes And personal direct taxes taxpayer.

RELEVANCE OF THE TOPIC

Russian tax system

Structure of Russian tax authorities

TAX HISTORY

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

HISTORY OF TAXES IN RUSSIA

FUNCTIONS AND TYPES OF TAXES IN THE RF

Functions of taxes:

The functions of taxes show how the social purpose of taxes is realized as an instrument of cost distribution and redistribution of income. Fiscal;

Regulatory;

Distribution;

Control;

Stimulating

TYPES OF TAXES IN THE RF

MAIN TYPES OF TAXES IN THE RF

Direct and indirect

. Direct taxes are levied directly on the taxpayer's property or income. These taxes are divided into real direct taxes And personal direct taxes taxpayer.

Fiscal;

Regulatory;

Distribution;

Control;

Stimulating

TYPES OF TAXES IN THE RF

MAIN TYPES OF TAXES IN THE RF

Direct and indirect . Direct taxes are levied directly on the taxpayer's property or income. These taxes are divided into real direct taxes And personal direct taxes taxpayer.

Regressive a tax is characterized by charging a higher percentage on low incomes and a lower percentage on high incomes.

Proportional tax, takes the same portion of any income (single rate for income of any amount).

Tax is considered progressive if the tax rate increases as income increases

Taxes levied from individuals ; taxes levied from enterprises and organizations ; related taxes , paid by both individuals and legal entities.

General taxes are used to finance expenses of state and local budgets. Special taxes have a purpose.

Indirect taxes are included in the price of goods and services. The final payer of indirect taxes is the consumer of the product. Indirect taxes are divided into indirect individual, And indirect universals

SOME EXOTIC TYPES OF TAXES

CONCLUSION

V.V. Putin: “Modern Russia needs a modern structure of the tax system. We should think about optimizing those taxes on which high-quality economic growth primarily depends.”

10 -11 grade

Completed by a teacher of technology, drawing, art

MBOU secondary school r.p. Multivertex

Nikolaevsky district, Khabarovsk Territory

Penkina Lyudmila Nikolaevna

Taxes are periodic forced payments by citizens from their property and income, going to the needs of the state and society and established by law.

Dictionary of Brockhaus and Efron.

Tax is a mandatory, individually gratuitous payment levied on organizations and individuals in the form of alienation of funds belonging to them by right of ownership, economic management or operational management for the purpose of financial support for the activities of the state and (or) municipalities.

Tax Code of the Russian Federation

Sun tax in the Balearic Islands This tax was introduced in the early 2000s. Since then, every tourist coming to the archipelago (Ibiza, Mallorca, Menorca and other islands) is required to pay one euro for each day of stay here. The funds collected through the “solar” fundraiser are used to clean the coastal zone and beaches of garbage, restore the ecological balance, that is, to improve the tourist infrastructure.

Beard tax

"beard sign" - a copper or silver badge with a Russian eagle on one side and the other and an image of the lower part of a face with a beard.

Beard tax

In 1535, King Henry VIII of England, who himself wore a beard, introduced a tax on beards. The tax turned out to be a progressive tax and depended on the social status of the taxpayer. His daughter, Elizabeth I, introduced this tax again, and only 2-week-old beards were levied on it. The same tax appeared in Russia, but for a different reason: it was levied primarily not to replenish the treasury, but because the tsar believed that bearded people looked like savages. How else to get people to shave?